.jpeg)

This article was written by Michael Wherry and first appeared on his Llinkedin on September 5, 2019. We loved it so much we asked for Michael's permission to share it with you here.

It has been a while since I [Michael] have sat in the conference room during lunch on Thursdays to discuss scheduling. Back in my CPA practice days, Thursday’s over lunch was the time that we got together to review schedules. Since then I have facilitated countless teams through process improvement projects and during each project the subject of scheduling comes up. Here is my take on scheduling: we don’t need it to the extent CPA firms are taking it.

In his book “The Goal”, author Eliyahu M. Goldratt discusses the five focusing steps. The five focusing steps are based on the premise that all processes are limited by at least one constraint. It is this constraint that limits the amount of work that can be completed over a given time. The five focusing steps are:

1. Identify the system’s constraint.

2. Decide how to exploit the system’s constraint.

3. Subordinate everything else to the above decisions.

4. Elevate the system’s constraint.

5. If in the previous steps a constraint has been broken Go back to step 1, but do not allow inertia to cause a system constraint.

Another way to say this is to focus your efforts on high value constraints, or obstacles, in your process. If you focus your efforts away from the high value obstacle you could be ignoring the core issue. When it comes to scheduling resources in CPA firms, scheduling is a lower value obstacle. Ask yourself this question: can I subordinate all work decisions based on the schedule created? I’d offer the answer to that is “no”.

The core issue most CPA firms are presented with is incomplete information received from their clients in order to begin work. This obstacle is where your resources should be allocated. How can you exploit the completeness of information received from clients? Begin working on client projects only when all necessary information has been received. Yes, you need to define what is necessary.

For attest engagements, request to receive all necessary PBC documents 1-2 weeks out from Fieldwork. The In-Charge should be responsible for verifying the client has provided you all your requested information at least 1-week out from Fieldwork. In doing so, it will allow you to complete fieldwork while in the field and who knows, you might also be able to leave the client with a draft financial statement before heading back to the office.

For tax engagements, ensure a substantial amount of information is in prior to routing to the Preparer / Analyst in the process. If you don’t, you’ll have hundreds of partially started engagements, nothing ready for the finish line, and chaos + wasted time in trying to manage that later.

The best of the best firms are spending the necessary time to ensure they receive all the necessary information to begin projects at the start. This concept is called a quick assessment. Ask anyone in your firm how quickly they can get something completed if they have all the information they need at the start of the project. I know I am stating the obvious, but CPA firms are notorious for doing the exact opposite. Very few are spending the necessary time to ensure we have received all the necessary information. Are your people working on things that can be completed with minimal pick up and put down? How complete was the information needed to complete that project before they began working on it? Focusing on quickly assessing the information received from your clients and reaching back out to ask for missing details pays immediate dividends. The quick assessment concept applies to all types of engagements; individual tax, business tax, advisory and attest engagements.

What good is the schedule if the client only sends in 15% of the information needed to complete the work? You and your team will be wasting tons of hours manually adjusting schedules instead of just getting the work done. Instead, once you ensure you have all necessary information before starting on projects, you will be amazed at how fast work can be completed by your team. With a lot less time “scheduling”.

The true obstacle in your CPA firm that requires significant attention is the request and receipt of client data. This should be one of your main focuses, not scheduling. Those who elevate scheduling to a top focus area don’t understand constraint management. Don’t chase the shiny object, instead focus on the root cause. Make meaningful progress towards receiving more complete information from your clients before starting work. Doing this will move your firm forward and elevate your client service.

To learn more about Michael Wherry and the work him and Dustin Hostetler are doing together visit https://transformityinc.com. We know you'd enjoy grabbing a virtual coffee with them as much as we do!

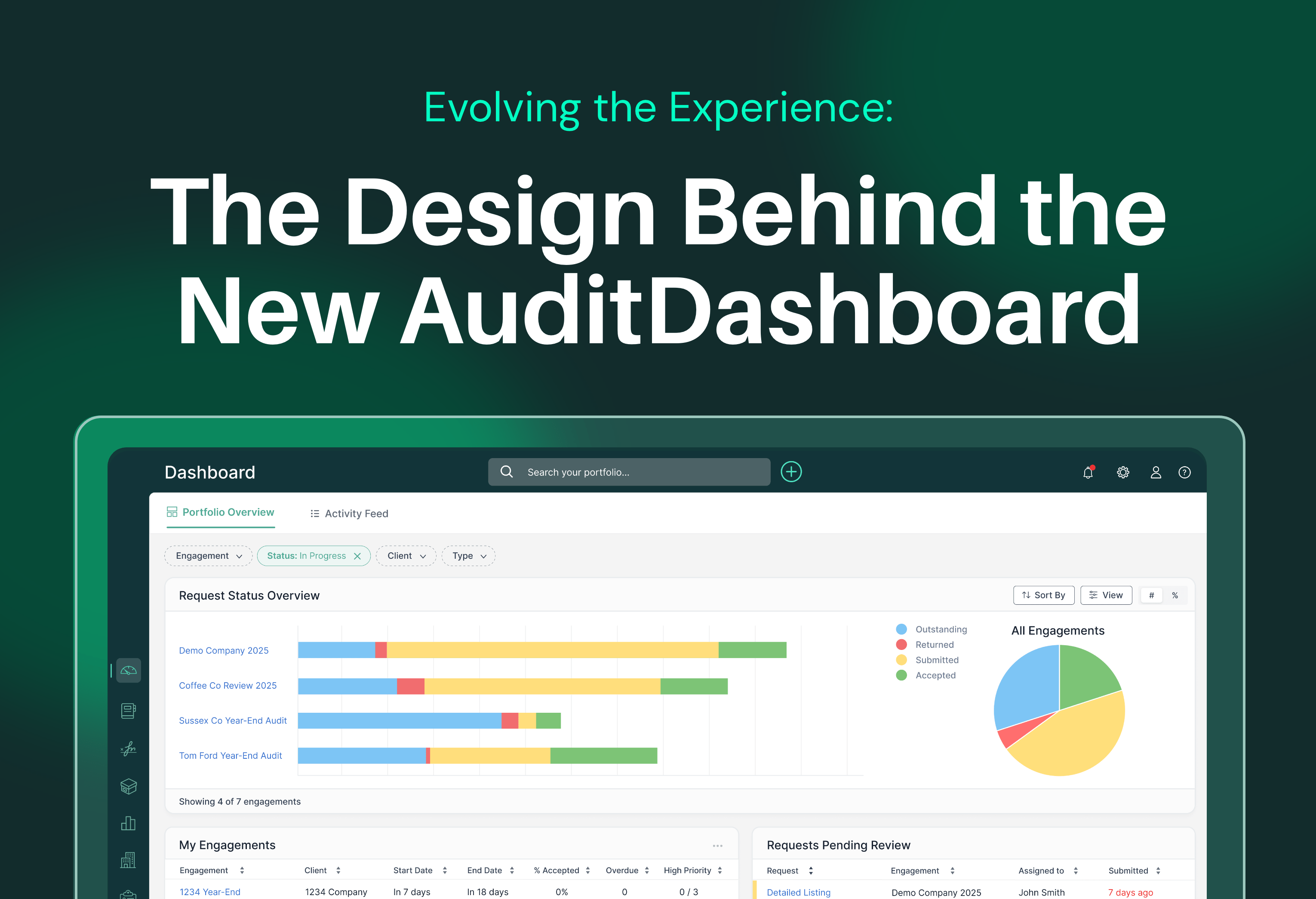

We began reimagining AuditDashboard’s interface with one goal in mind: to modernize the experience while preserving the familiar workflows users depend on every day. Guided by years of meaningful customer conversations, we approached every decision with purpose and care.

Read moreRead more

Traditional audit scheduling often leads to delays, inefficiencies, and client frustration. This post introduces a smarter, more agile approach: triggering fieldwork when 80% of client requests are completed. Learn how this shift improves utilization, momentum, and client collaboration — and how AuditDashboard helps firms make it happen.

Read moreRead more

Busy season is upon us, and just like last year, it’s guaranteed to bring unique challenges and a few unwanted surprises. If you don’t adopt strategies to manage the overwhelm, heavy workloads, tight deadlines, and endless client requests will derail your productivity. While there’s no magic wand to buying back your time or making it all disappear, these five strategies will make this audit season more manageable and less stressful.

Read moreRead more